The United States and Israel have launched an unprecedented joint air campaign against Iran, targeting senior leadership, nuclear facilities, ballistic missile sites, command infrastructure, air defence systems, and naval assets.

Supreme Leader Ayatollah Ali Khamenei has been confirmed killed, which will lead to only the second change of Supreme Leader in the Islamic Republic's history. In response, Iran has launched retaliatory strikes across the region and effectively closed the Strait of Hormuz - a critical waterway through which approximately 20% of global oil and 25% of LNG flows daily.

This brief note from the Prosperity Investment Committee examines the economic implications, market risks, and investment considerations arising from these developments.

What Has Happened?

Following a prolonged diplomatic impasse over Iran's nuclear program, ballistic missile development, and regional proxy activities, the US–Israel joint campaign has targeted a broad range of assets. The killing of Khamenei, along with numerous senior regime figures, marks a profound geopolitical inflection point, one that sets in motion succession dynamics with deeply uncertain outcomes.

Iran's retaliatory strikes have targeted US assets and civilian infrastructure across Israel, the UAE, Saudi Arabia, Kuwait, Oman, Jordan, Iraq, Qatar, and Bahrain. Regional airspace has been significantly disrupted and the Strait of Hormuz closure has removed approximately one-fifth of global oil supply from markets, with no clear timeline for restoration.

Impact on Global Markets

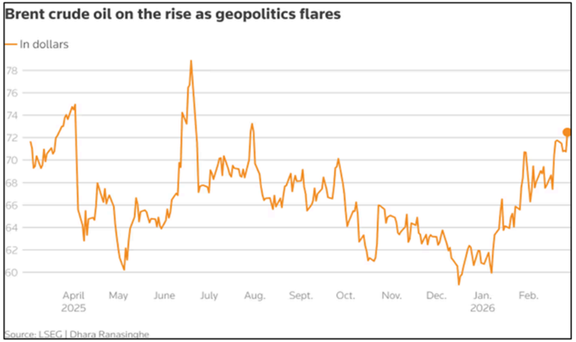

The most immediate and significant market transmission mechanism is energy prices. Oil prices, which had already risen to approximately USD $72 per barrel following the commencement of hostilities, face the prospect of further material upside should the conflict persist or escalate.

Key market considerations include:

Oil price risk: A sustained disruption to Strait of Hormuz flows could drive oil prices substantially higher. While OPEC+ nations hold approximately 3.5 million barrels per day of spare capacity, this is rendered largely academic if the Strait remains blocked.

Additional commodity risk: Oil is not the only commodity that passes through the straight. Closure could severely disrupt the flow of LNG and fertiliser exports from Gulf producers, triggering sharp increases in diesel, ammonia and urea prices. These are key inputs for broadacre cropping and intensive agriculture. The resulting input cost inflation and freight bottlenecks could compress farm margins, delay planting decisions, and likely translate into higher global food prices, particularly for import-dependent regions in Asia and Africa.

Inflation and interest rates: A significant oil price surge would add to inflationary pressures globally. However, the relationship between oil prices and central bank policy is not straightforward. Central banks will look through supply-side shocks to the extent they do not become embedded in underlying inflation expectations.

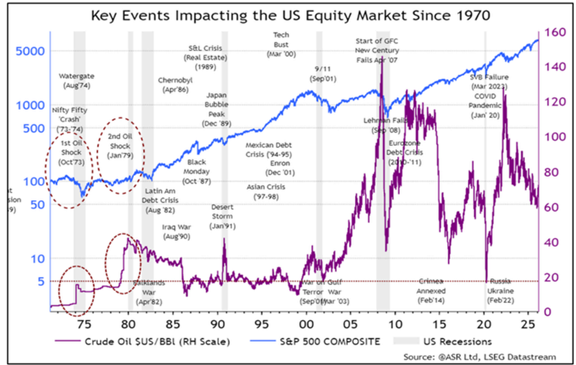

Equity markets: Global equities face headwinds from heightened geopolitical risk and growth uncertainty. History suggests share markets typically pull back sharply on geopolitical shocks before recovering once clarity improves.

Safe haven assets: Gold and government bonds are likely to benefit from a flight to safety. Energy sector equities may see support from higher commodity prices.

Insurance and sovereign risk: Low-cost Iranian drone penetration of Gulf airspace challenges assumptions previously held about the safety of commercial hubs such as Dubai and Doha, with near-term implications for aviation, property valuations, energy infrastructure insurance, and sovereign risk premiums.

Regional medium-term outlook: Notwithstanding near-term volatility, Iran has historically been the single greatest obstacle to the Middle East's ambitions as a global hub for finance, technology, tourism, and trade. A materially weakened Iran whether through regime change or prolonged internal instability may, over the very long term, serve as a structural positive for regional integration and investment over the medium to long term.

Impact on Australia

For Australian investors and households, the primary transmission channel is likely through higher petrol prices. Australian petrol prices track the Asian Tapis benchmark closely, which in turn tracks US oil prices.

AMP’s research suggests that as a broad rule of thumb, for every USD $1 per barrel rise in oil prices adds approximately one cent per litre to domestic petrol prices. Accordingly, a USD $40 per barrel rise in world oil prices taking prices above USD $100 per barrel, would add approximately 40 cents per litre to petrol prices, with a 7–10 day lag if sustained.

On average, household consumption of approximately 35 litres per week, this would add roughly $14 per week to the household petrol bill, acting as an effective tax on consumer spending and dampening broader economic activity. A 40 cents per litre rise in petrol prices would add to inflation. For the Reserve Bank of Australia, the implications are somewhat ambiguous.

It is worth noting that Australia is relatively well-positioned as a net energy exporter. Higher gas and coal prices may provide an offsetting economic benefit, and our economy is less oil-dependent than many developed market peers.

Scenarios

The trajectory of the conflict remains highly uncertain. It will depend primarily on Iran's capacity to reinstate senior leadership and maintain regime cohesion, following the loss of Khamenei and numerous senior figures.

At one end of the spectrum, the strikes may prove a tipping point for a regime already under significant internal pressure, producing a period of domestic instability and fragmentation. While disruptive in the near term, this ultimately reduces Iran's ability to destabilise the region.

At the other end, residual regime structures survive. Iran retains meaningful missile and drone stockpiles, the conflict settles into a prolonged war of attrition and ongoing costs for the US, Israel, and Gulf states.

The tail risk worth monitoring, is deliberate escalation targeting Gulf oil infrastructure or Strait of Hormuz shipping, this scenario would draw in additional regional actors and carry a meaningfully higher probability of miscalculation.

What history suggests is that the range of outcomes is wide, the situation will evolve quickly, and early assessments (including this one) are likely to be revised. The more useful framing for investors is not which scenario prevails, but ensuring portfolios are resilient across the range of plausible outcomes.

Implications for Investors

Our strategic asset allocation was only recently updated and implemented. Our investment committee constantly looks for opportunities when they present. Volatility in markets is an example of this. If we believe the impacts will shift fundamentals and valuations, we will continue to act.

If you have any questions about the above, please call your Prosperity Financial Adviser on 1300 795 515 to discuss.